What are the risks for FCPA?

Besides the FCPA, there’s also UK Bribery Act, and other things like Germany, the anti-corruption law in China, and all these things. So what is it about the FCPA that we need to be careful about? Basically, what it is, is we’re going to get massive fines. So we have to be really careful about whether or not we’re going to get a big fine from the SEC when we are having non-compliance with the FCPA.

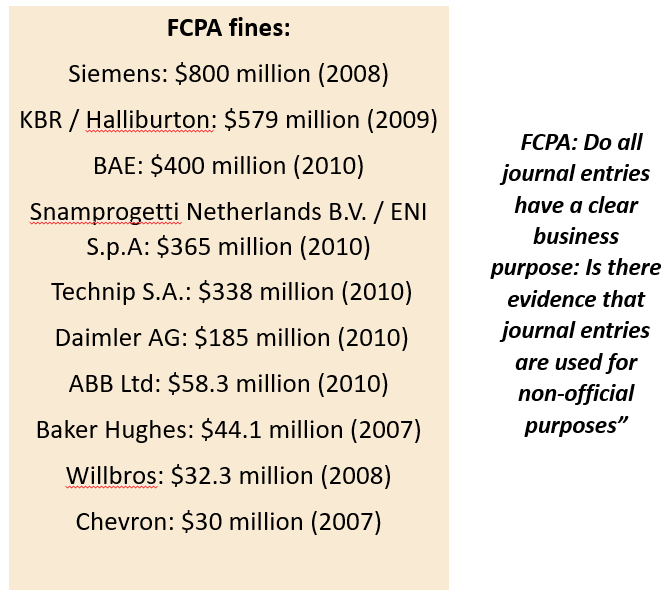

So for example, Siemens, they get an 800 million fine in 2008, and it just goes on and on and on. These are quite old figures. Technip got a massive fine in 2010, Daimler, ABB, like there are lots of companies out there, huge fines from the SEC because of FCPA.

And it’s not only what they’re doing in the US, it’s actually what they’re doing in foreign countries. But because they are listed on the US or because they have to report to the SEC, this is why they are considered to be under the FCPA. So if anyone in any of those entities around the world gives like some money to a foreign official, and they’re doing that to get an unfair strategic advantage or an unfair commercial advantage, then this is where the SEC will give you a fine.

So what do we mean by foreign official? Basically, a foreign official is anybody that works in a company that’s owned by the state, or it could be partly owned by the state. And it could also be anybody that actually does work for the state. So if it’s a customs officer, if it’s a political person, or if it’s a state owned enterprise, even if it’s only like 10% state owned, and you are giving a bribe to somebody in that company, then it can be under the FCPA.

So it might be for example, like you are making trains. And in China, you want to give a little bit of a bribe like a present or something to the government or government official or a state owned enterprise that you’re working with in order to get those trains built for China, right, massive project, whatever it is, if you’re giving a little bit of money or a present or something like that, and you’re giving somebody who’s working in a state owned enterprise, you might think it’s not state owned enterprise, it might sound like it’s just a private enterprise. But if you’re doing something like that, then it can be considered to be a bribe or doing something to get an unfair advantage.

If you’re doing that, then the SEC can give you a massive fine under the FCPA. So what’s the SEC going to do like SEC, basically, they’re going to get a tip off, somebody is going to tell them that something’s going on, right, because you can actually get a reward. And if SEC will give out rewards for people who are giving them tip offs, and it will be a percentage of the fines, it’s actually quite a huge reward that people get for giving the SEC a tip off.

So the SEC is going to get a tip off. And then what they’re going to do is they’re going to show up. And when they show up, they’re going to do a whole load of testing, right, they’re going to whole load of testing, and there’s a whole lot of data analytics, especially data analytics, because they are in it to find out for real, right, they’re not just auditors that are going to come out there and do a few interviews and then go home. No, they want to find out.

So if they’re serious about finding out, and they’re going to do some data analytics, and this is really one of the things that really goes to show that data analytics is so essential for audit, it really is 100% essential. So the SEC are going to show up, and they’re going to do some data analytics, and they’re probably going to ask for all of the journal entries for the last like five, six years.

They’re going to go through and they’re going to check for loads of things. And in the FCPA law, it says, and it’s the same in the SAPIN II, and it’s pretty much the same in the UK Bribery Act, and all the others, they can ask themselves questions like, do all of the journal entries have a clear business purpose? Is there evidence that journal entries are used for non-official purposes? It means like, do you have a journal entry somewhere in your general ledger? That doesn’t make sense, right? So what does that mean? So it’s like, normally, you’ve got entries in there that are coming from operations, like you’ve your supplier invoices, and supplier invoices are coming from the MM module. And you’re going to get those into your general ledger, and they’re going to be from the MM module, because they’ve gone through purchase orders, approvals, and then you’ve had some good receipts, and then you got the invoice, enter the invoice, and then it’s been approved, it’s been like a three-way match, and then there’s the payment and all of that.

And that would be a normal journal entry for a supplier payment, supplier invoice. But if you have entries in your general ledger, for example, you just have bank out, if you just have bank out, and there’s nothing that is matched, like it’s not clear to an invoice, then that would actually be what we call an unsupported journal entry, because no documentation, and it’s not for official purposes, not for official business purposes.