FCPA data visualization - part 1/4

Over the years I’ve been an ACL like super expert at Deloitte for 10 years.

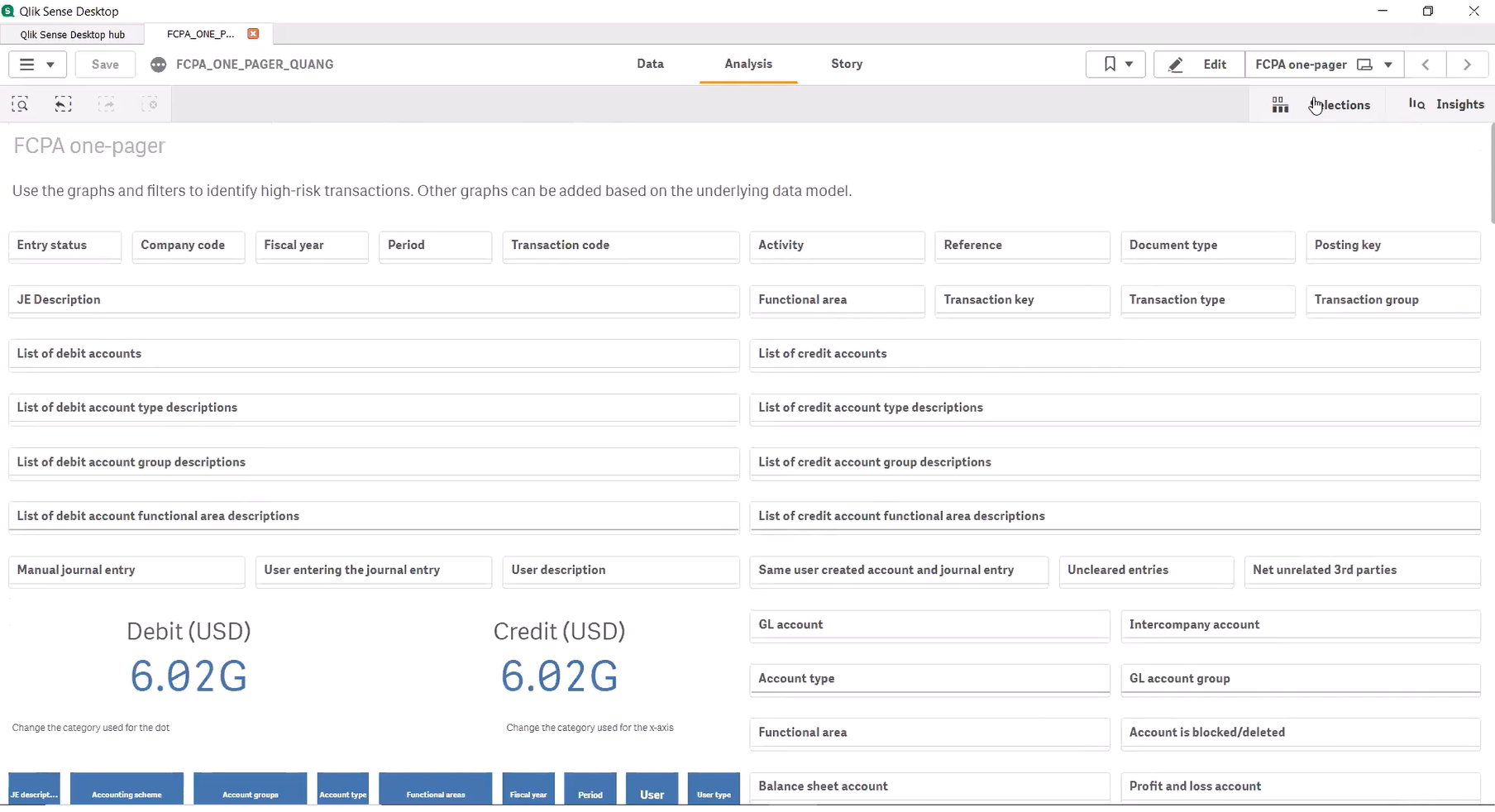

Those systems that start to get some visualisation, but you need to really these days people want one pager because they’ve got much time and they also want visualisation. So what I’m going to do is I’m going to walk you through this dashboard and behind the scenes in the Qlik App, you’ll actually be able to see all of the code as well. So over here, you have a load of stuff about the general ledger. And this is really exciting. Like it looks just like filters and things, but it’s actually really exciting. So here you’ve got your list of debit accounts and here you have your list of credit account

So what’s really interesting when we want to check the accounting records, right? So we are saying we want to check that we’ve compliant with FCPA, compliant with UK Bribery Act, whatever it is. One of the main things they say is that they have accurate journal entries, accurate accounting records. So we want to make sure that our accounting records are accurate.

And we talked about the Top 10 data analytics for fraud detection. The first one was journal entries because when you’re doing a journal entry, if you’re doing it manually, then you can basically enter whatever you want. So we want to be able to check the journal entries.

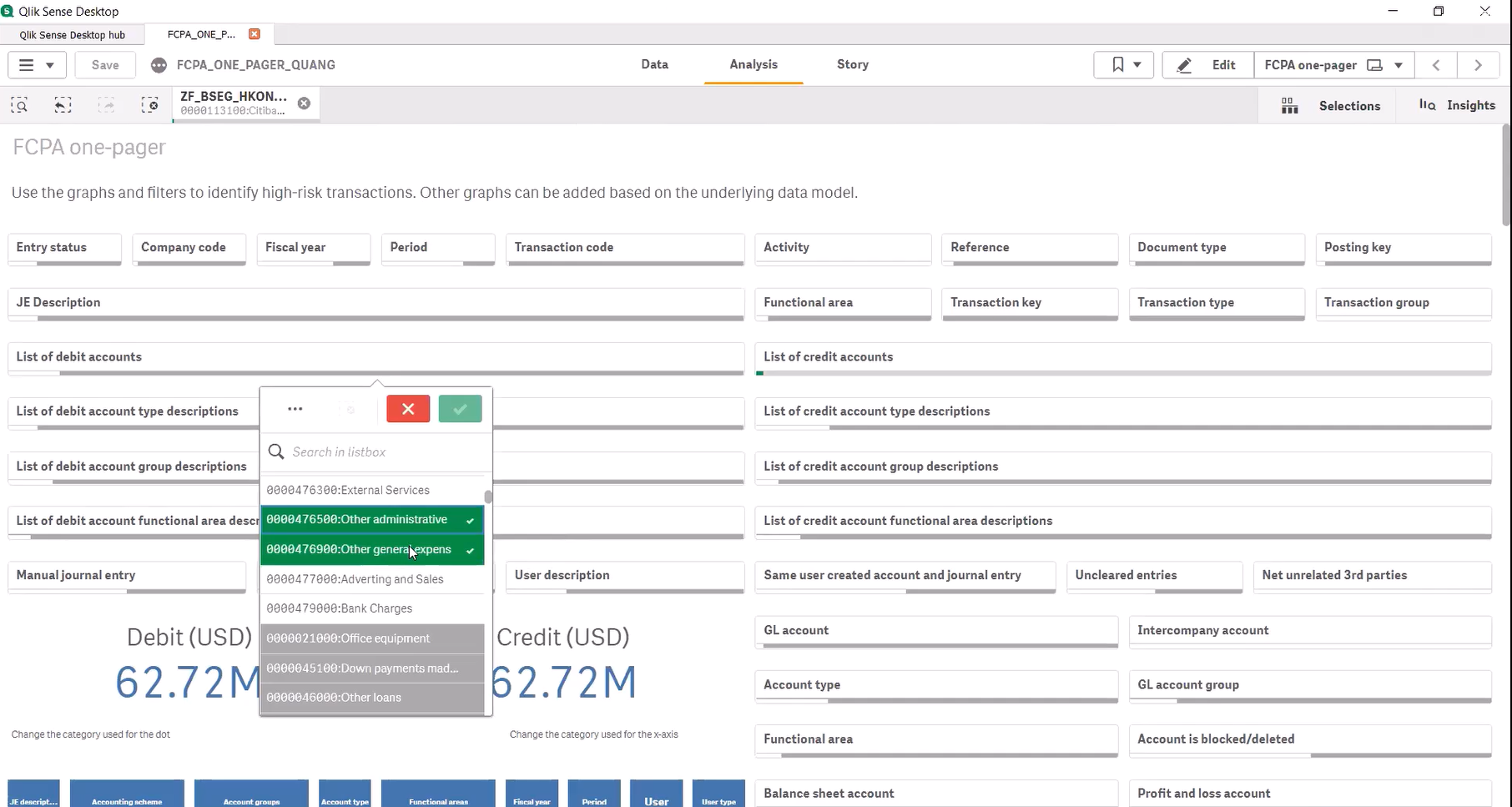

We want to be able to check the accounting schemes. And so, for example, here you’ve got the bank. This is the general ledger account for bank.

You can see you’ve got Citibank, you’ve got Deutsche Bank, whatever it is. And now if I select on the credit the bank, so since bank is an asset, this means that the money is going out of the bank, right? It could be going to another bank account, you know, depending on what we have on the debit side, see that in a minute, but it’s going out of Citibank. And if we wanted to analyse this, so there are different ways.

So one way is just a simple bank out transaction. And if you’re doing a manual journal entry, you can write. So here we do credit the bank. And on the debit side, we can check what kind of transactions do we have on the debit side. So if I click on the debit filter here, I’m going to be able to check if I have a cost account.

So if I go down down this list, I’ve got the lists. And this is actually the list of general ledger accounts that are found in the same journal entry as a bank out from Citibank. Okay, I’m going to debit a cost account and credit the bank. It’s not actually normal if you debit cost credit bank and it’s like, for example, you debit sundry expenses, and then you credit bank, because if you do that, you don’t really have any traceability. It’s like, why did you send that money out of the bank? You’re just putting it on sundry expenses, but you don’t actually know who is the beneficiary and what was the reason for doing the payment. And this is why in the FCPA, they say that all of the journal entries need to be supported and they need to be backed up.

They have to have a real business purpose. And so we can look for things that look strange, like, for example, other administrative, this is other administrative costs. And you can see here that there is only one general ledger account written. There’s no list of other accounts on the debit side for this type of journal entries. So it means we just got cost and bank.

This one is other general expense. So what I would do is if I wanted to see if we’ve got some strange things in here, so straight away, go into the bank general ledger accounts, especially if I know what they are, and see what they are on credit, because that would be bank out. And then look for some generic cost accounts on debit. I can then filter on that. I’ve already got some strange journal entries. I can see that it’s $2.5 million. So it’s quite a significant amount. I mean, that would definitely get you a fine from the FCPA if somebody has taken this money out of the company, and then they’re using it for a bribe. I mean, because anything over like, you know, $50,000 or something that’s that’s easily going to be working as a bribe. So here, we’re talking about quite a lot of money going out of the bank, and it is debit cost. That is something that we should definitely look at if we are an auditor. So that’s just taking me two seconds to check, right? There’s so many things on here that we can talk about that we could check. But this is the most like essential thing that I would check.

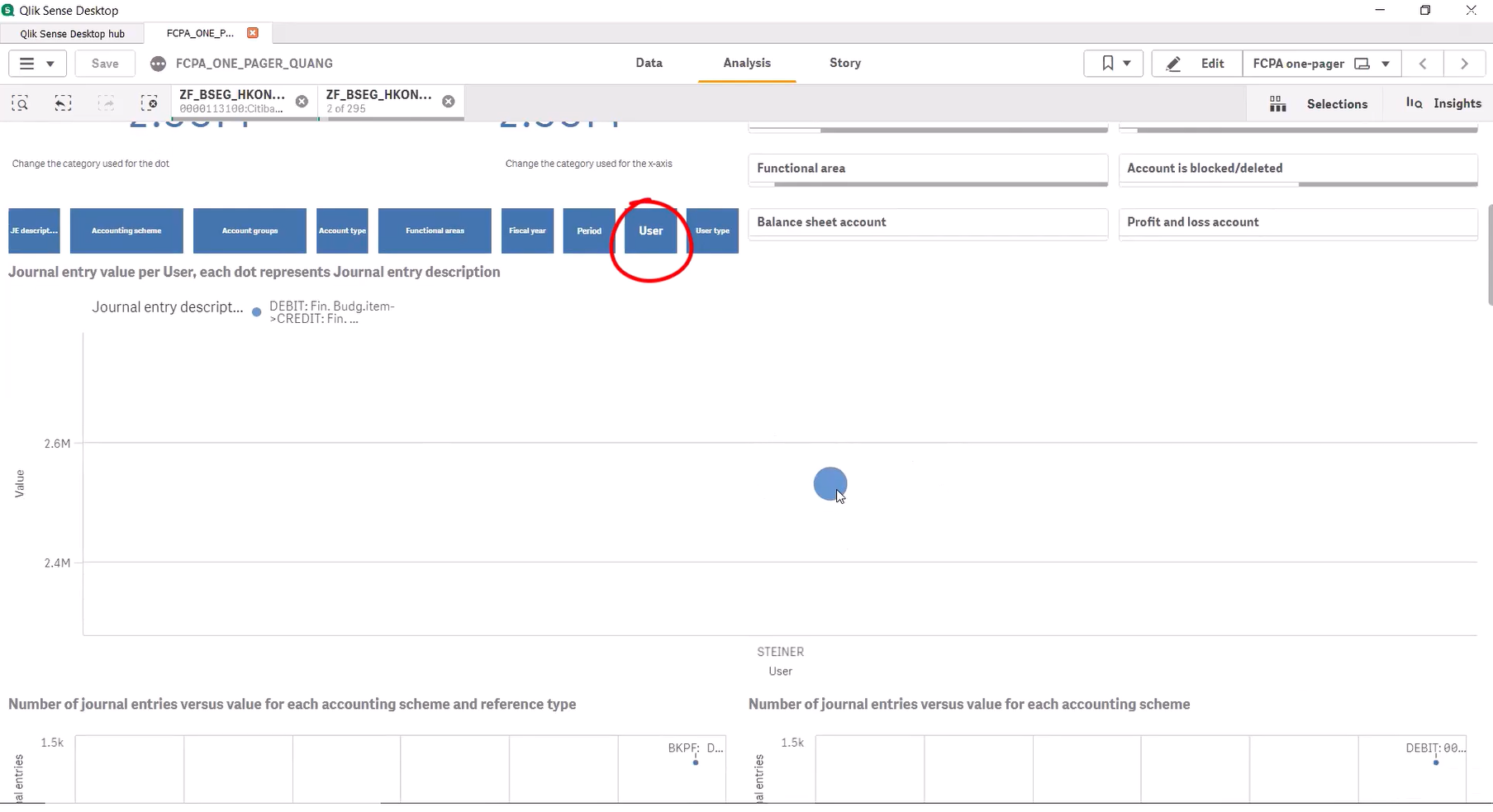

And not only this journal entry, this is like what we call an accounting scheme, right? Not only this accounting scheme, but this is quite an interesting one. And so after that, once I’ve filtered on that, I can come down, I can have a look at this graph down here. So down here, we have a graph, and we can see straight off, who is the user. So here, we’ve actually clicked on the user button. So we’re seeing who the user is actually entered these types of transactions. So we got that immediately that information.

And then since we know already is only one user, maybe I can click on the period, because maybe I would rather see, you know, is he doing that all the time? Or is that just something that’s happening on a one off situation? Alright, so if I click on the period, now you can see that the dimension has actually changed, like the category down here on the x axis is changed to period. And now what I’m seeing is that these are things that are happening over time, he’s posting all these things over time. So maybe it’s just an adjustment or something, but it’s still a bit strange, it could be a foreign exchange adjustment.